Construction company with TowerCo that could be worth the entire market cap today

An ASEAN watchlist item I'm monitoring closely

Disclaimer: The following post is not investment advice, please do your own due diligence. If you think I am wrong, please challenge me

This is a preliminary discussion on a construction company with a rapidly growing cell tower leasing business that is set to dominate Vietnam’s 5G rollout. In under 5 years, I expect the operating earnings of their cell tower business alone to be equal to the 2024 EBIT of all the company’s business segments combined.

Note that I have not initiated a position. But it’s a strong watchlist item that I will be monitoring closely.

CTR trades at 21x 2024 earnings which I think is a bit too high given the risks involved. But there a lot to like and still worth discussing!

I’ve previously wrote about the rapid growth Vietnam has experienced from the China + One trend where factories are near shoring new factory capacity in Vietnam due to the cheap labour, proximity to China, and more favorable US relations. Vietnam today is one of the fastest growing economies with FDI and trade shooting through the roof.

I’ve spent the past months searching for Vietnam businesses that can absorb this growth to add to my portfolio.

Infrastructure was the first that came to mind.

However, the one problem I’ve found with these businesses is that most of them are almost 100% owned by the state.

In a lot of cases, there is no incentive for the business to increase profits, even though they are natural monopolies, instead prioritizing public good even if it means operating at a loss.

You see, these businesses typically do not own the underlying infrastructure assets, the state does.

For example, most ports run on concessions to operate the port and do not own the port itself. If the government has a problem, they can revoke the concession.

Additionally, the government might build a new port right next to an existing one and retire the old one. As such, single-concession port companies have no guarantee they can maintain their monopoly.

Railways face a different issue.

The Railway Transport JSC (UPCom: TRV), which owns most of Vietnam’s passenger railways, have indefinite usage rights but do not own the tracks or land underneath the tracks. The state simply allows TRV to operate the cars on the tracks. TRV has no control over pricing or track expansion. As such, though they have no direct competitors, they do not get to exercise the advantages a monopoly would normally have.

But!

There was one kind of infrastructure play that I think deserves just as much attention…

If there’s anything you can learn from quickly growing markets, it’s that one of the most important transformations a country needs to make to sustain its growth is to adopt strong telecom infrastructure. I’m talking cables, transmission lines, broadcast stations, cell towers.

As business and trade grows and people start living in a modern interconnected economy, data and wifi and communication is everything.

So let me tell you a story…

")

It’s the 90s — The United States had recently released Vietnam’s embargo and Vietnam’s relations between China and the US had normalized. The country was in full Đổi Mới reform with the goal of creating a socialist market economy.

VNPT or VinaPhone, the 100% state-owned telecom operator, was a mandated monopoly and controlled all telecom infrastructure in Vietnam.

But 1995 would change everything.

Facing pressure to create a more competitive telecom industry, the state allowed the creation of other state-owned telcos. This led to the formation of Viettel, owned the Vietnamese Military, as well as Saigon Postel, owned by VNPT and 10 other state-owned shareholders.

Furthermore, the government opened up the sector to foreign investors. This led to the creation of several new telcos most notably Mobifone by Comvik via a cost-revenue sharing agreement with the government.

But due to restrictions placed by government, such as all players being forced to use VNPT-owned infrastructure, which maintained the state-driven dominance of VNPT, as well as the severe price-cutting competition sparked by the flow of new entrants, the economics broke down and by 2012, nearly all foreign players were gone.

Comvik got out after their agreement expired, which led VNPT to acquire Mobifone, though the state mandated VNPT to separate Mobifone as a separate company with ownership transferring to CMSC, another government body, in 2018.

Though VNPT continues to maintain control over fixed transmission line, as the mobile market would come to dominate, it allowed new entrants to build mobile network infrastructure not monopolized by VNPT.

Today, Vietnam’s mobile network is dominated by 3 operators: Viettel, VNPT, and Mobifone.

These three operators (or MNOs) make up over 90% of the entire market.

You will notice Viettel has risen as the market leader, by a significant margin.

But why?

Weren’t Viettel, VNPT, and Mobifone all wholly state-owned companies?

The answer has to do with Viettel’s connection to the military of Vietnam.

Why was Viettel so successful?

You see, while the typical state-owned business was slow, bureaucratic, and hierarchical, I’ve found that Vietnam’s military-owned businesses have displayed a culture and organization that is fast, performance-driven, and meritocratic.

This was no different for Viettel.

Performance evaluations were based on hitting KPIs. On the other hand, traditional state-owned companies were content with just giving out salaries.

Ex-employees described Viettel’s culture as one of military-like discipline. Employees were expected to push as hard as they can to reach their goals and many worked long hours.

Nevertheless, structure was not too hierarchical — innovation and ability were prized with Viettel often paying highly to reward and retain excellent talent.

When Viettel entered the telco space, they acted fast to dominate the rapidly growing mobile demand with new technology whereas VNPT had continued to depend on older systems as their monopoly and infrastructure control endowed them with high margins, margins that would erode as soon as aggressive operators began charging half off.

Secondly, Viettel knew they couldn’t win fighting VNPT in the cities, so they had to focus on the underpenetrated countryside which allowed it to extend its mobile network nationwide. VNPT and Mobifone would later be forced to play catch up.

There were many other benefits of having the military to back you up:

→ The military’s goals of strengthening the army and its intelligence incentivized Viettel to focus on R&D and foreign partnerships, supplying best-in-class equipment for the business where they could be good enough for military use.

→ The military’s power over the government enabled them to lobby against VNPT’s anti-competitive practices, which influenced the increasing liberalization and pro-competitiveness of the entire telecom industry.

→ The military’s extensive land network (bases, stations, etc) and hard working military-trained workforce allows Viettel to build faster than all other competitors and provide undisputed access to land rights to build towers and infrastructure where other competitors were still forced to rely on VNPT’s infrastructure due to high CapEx requirements.

In other words, you could make the argument that being owned by the military was itself already a moat due to a combination of the culture and access to hard-to-get political and physical resources.

This leads me to the company I want to discuss today.

Meet Viettel Construction (HOSE: CTR), a subsidiary of Viettel Group, valued at roughly $450M USD trading at 21x after-tax 2024 earnings with net cash position about 8% of market cap.

CTR’s main business is operating and maintaining Viettel’s towers, lines, and network. Nearly 40% of revenues comes from the telco operations segment and Viettel Group is really the only customer.

Then we have the construction business. This segment is involved in building, installing, and reinforcing stations, antenna poles, television poles, lightning protection grounding systems, fiber optic cable systems, and more.

They are also involved in various construction projects in real estate, civil works, and industrial parks serving a variety of non-Viettel. Construction accounts for close to 25% of revenues.

Above: 1 year 270 billion VND Suburban 5A project for CDC Real Estate completed in December 2024.

Above: 1.5 year 271 billion VND An Dien Project for Eco Pearl JSC scheduled for completion by May 2026.

About 14% of sales come from Myanmar and Cambodia related to constructing and operating Viettel’s network in those countries, so that belongs to the construction and operations segments. Additionally, CTR is also involved in other businesses ranging from solar panel installation to IoT distribution.

However, what I’m really interested in is their Cell Tower leasing segment.

These towers act as leasable passive infrastructure on which MNOs will place their telco equipment to be able to provide mobile data coverage. A tower is not simply just a piece of steel but also the fiber cable wiring, rack space, etc. CTR makes money by charging tenant MNOs monthly for the space to place their equipment on it. Towers can come in the form of larger stand-alone towers (macro or ground-based) or small cell/rooftop towers, which are more common in the city.

This segment was started in 2020 when Viettel announced a push towards sharing network infrastructure.

CTR builds and, importantly, OWNS the towers and leases them to Viettel and other MNOs.

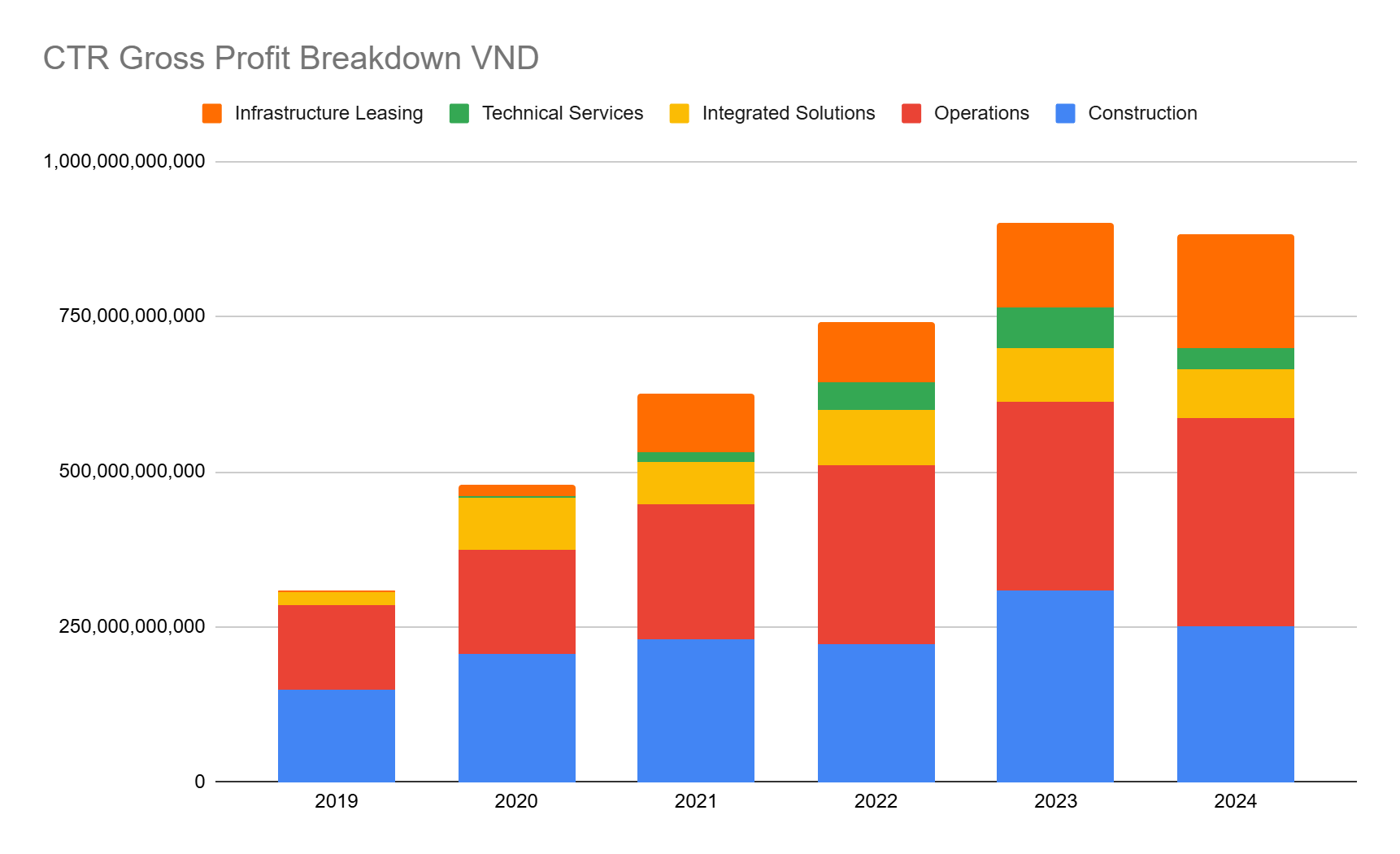

In just 5 years, the tower co went from 0.5% of revenue to 5%, and from <4% of gross profits to over 20%!

While the core construction and telco operations segment have grown gross profits at about 5% and 19% respectively, the tower co has grown profits at a whopping >75% CAGR!

CTR’s towers are largely in areas uncovered by Viettel Group’s existing tower network or places that require densification to accommodate more traffic. In bigger cities, CTR may own up to 20% of Viettel towers.

In other words, CTR is Viettel’s primary vehicle of 1) extending coverage nationwide and 2) deploying 5G

Source: MBS Research

I believe CTR’s tower co possesses the following properties:

1) a long growth runway as Vietnam’s 5G penetration is still just 25% with government mandates of 99% by 2030. Due to 5G’s shorter wavelenghts, Vietnam will probably need somewhere in the range of 100-200,000 more towers to reach total coverage.

2) a 10% lower cost base than peers due to the vertical integration + scale advantages

3) and tower economics that could reach >30% ROIC due to the high incremental margins and high switching costs.

CTR already owns >12,000 towers and aims to build 2,500 towers a year, a 15% 5 year cagr in tower count growth. I estimate the rollout to be 50% of Viettel Group’s annual total tower expansion goals in Vietnam.

Now let’s discuss what makes cell towers such a good business?

High predictable recurring revenue

As telecom operators optimize their network coverage, switching to another nearby tower would require you to re-optimize your network coverage, risk potential downtime which would frustrate your subscribers, and you would also have to spend to transfer active equipment from one tower to another (note that I do not yet know the exact figure). Contracts typically last 5-10 years with price escalations. Prices may increase 5-10% at renewal.

As a result, there is little reason to switch to a nearby tower even if a competitor might offer a better price.

High incremental margins

Towers can accommodate multiple tenants/telecom operators and the cost of having one tenant is almost the same as having two or three → operating leverage!

Most countries typically have about 3-4 dominant telecom operators, as such in most cases a tower can at most take in 3-4 tenants. High consolidation will lead to lower tenancy and hurt margins.

Currently, most telecom operators in Vietnam operate on their own towers, though the state has recently expressed the desire to have operators share their tower infrastructure going forward.

If Vietnam’s operators decide to share their future towers, the tower co tenancy ratios will go up and so will their gross margins.

Access to scarce locations.

Towers are often subject to local and regulatory pushback as they don’t look pretty and residents fear side effects or externalities like radiation, lightning strikes, or large fires.

I’ve founded plenty of evidence for strong local “Not in my backyard” situations where towers would face significant backlash from residents claiming it may invite lightning strikes, cause health side effects, and more.

Nevertheless, there remains no official regulation in Vietnam preventing you from building a tower right next to an existing one. And enforcement is inconsistent with evidence to believe some towers from all players lack the proper permitting and instead use political connections to build.

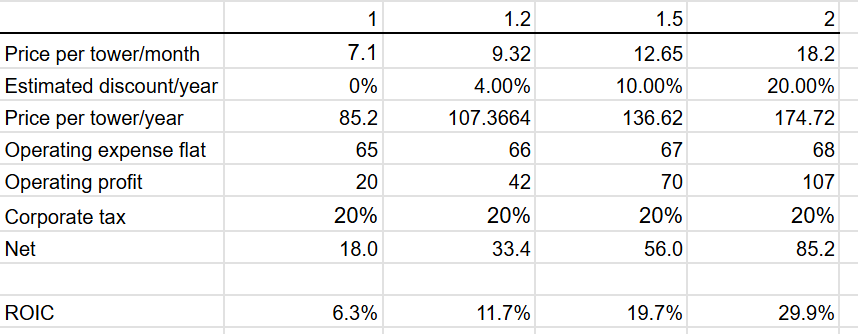

The picture below shows my brief breakdown of CTR’s tower economics:

If CTR is able to add ~0.5 average tenants/tower, i.e. the tenancy reaches ~1.5, ROICs crack 20%. And adding ~1 whole average tenant/tower brings ROIC to 30%.

As you can see, tenancy is the biggest lever for this thesis to work. Right now, since most towers still only have Viettel as a tenant, i.e. tenancy is close to 1, ROIC per tower today remains quite low. But as the country develops and based on the rhetoric I’m seeing from the state, I think 1.5x is within reach, dare I say inevitable. For reference, competitor OCK Vietnam already has a tenancy of 1.4x.

Essentially the key factors influencing tenancy overtime are:

1) high CapEx requirements for expanding coverage, which will be massive due to the 5G rollout

2) regulation against tower duplication and

3) high competition which will force MNOs to lease to reduce upfront costs and replicate each other’s coverage. (But not too high as we’ve seen in India where too much competition can force many players into bankruptcy leading to high tower vacancy).

I would need to publish an entire post to talk about this in detail covering the history of other telecom industries in other countries but suffice it to say I think CTR is on the path to 1.5x and my base case assumptions assume 1.5x tenancy within 5-6 years. I think 2x possible but no guarantees.

Competition

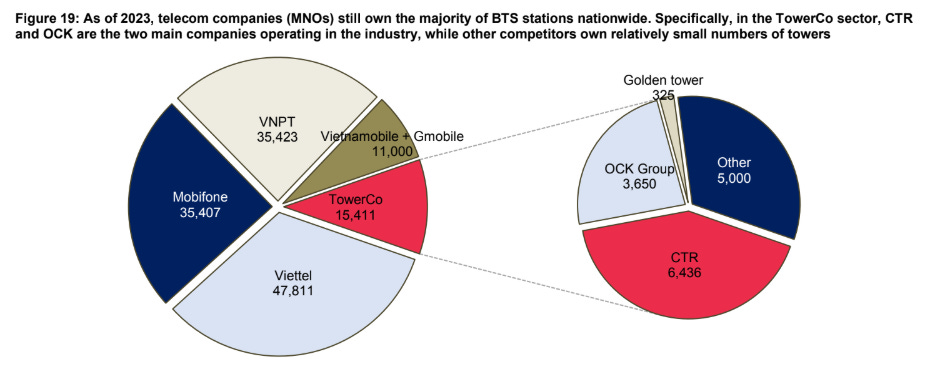

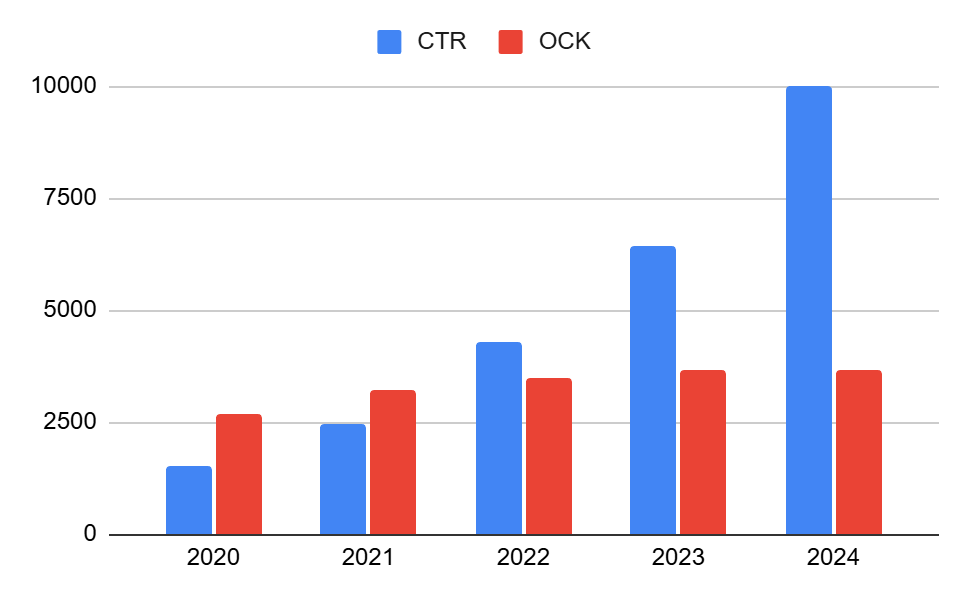

In Vietnam, CTR is the largest tower co, followed by OCK, an international tower portfolio, and other small players.

Independent tower cos like OCK have usually opted to acquire rather than build and despite OCK historically being the largest tower co, they have in recent years seen far slower tower growth compared to CTR.

But why has CTR left OCK in the dust? From my conversation with an ex-OCK employee, I learned that OCK didn’t want to deal with the politics. Building towers meant you need connections, friends in high places, or be forced to give hefty bribes.

Since OCK did not want to deal with that, they opted for acquisition, but even then it was simply worth focusing more in countries like Malaysia where OCK had better expertise.

On the other hand, Viettel has been explicit about it’s aggressive tower plans.

Chairman and General Director of Viettel Group Tao Duc Thang has emphasized the importance of CTR’s position as the top tower co:

“Viettel Construction must continue to maintain and firmly affirm its position as the No. 1 TowerCo in Vietnam. This is not just a target of scale or market share, but a strategic requirement associated with Viettel’s responsibility in ensuring infrastructure for socio-economic development and defense and security tasks in the new period.” - Lieutenant General Tao Duc Thang at the Military Conference 2025

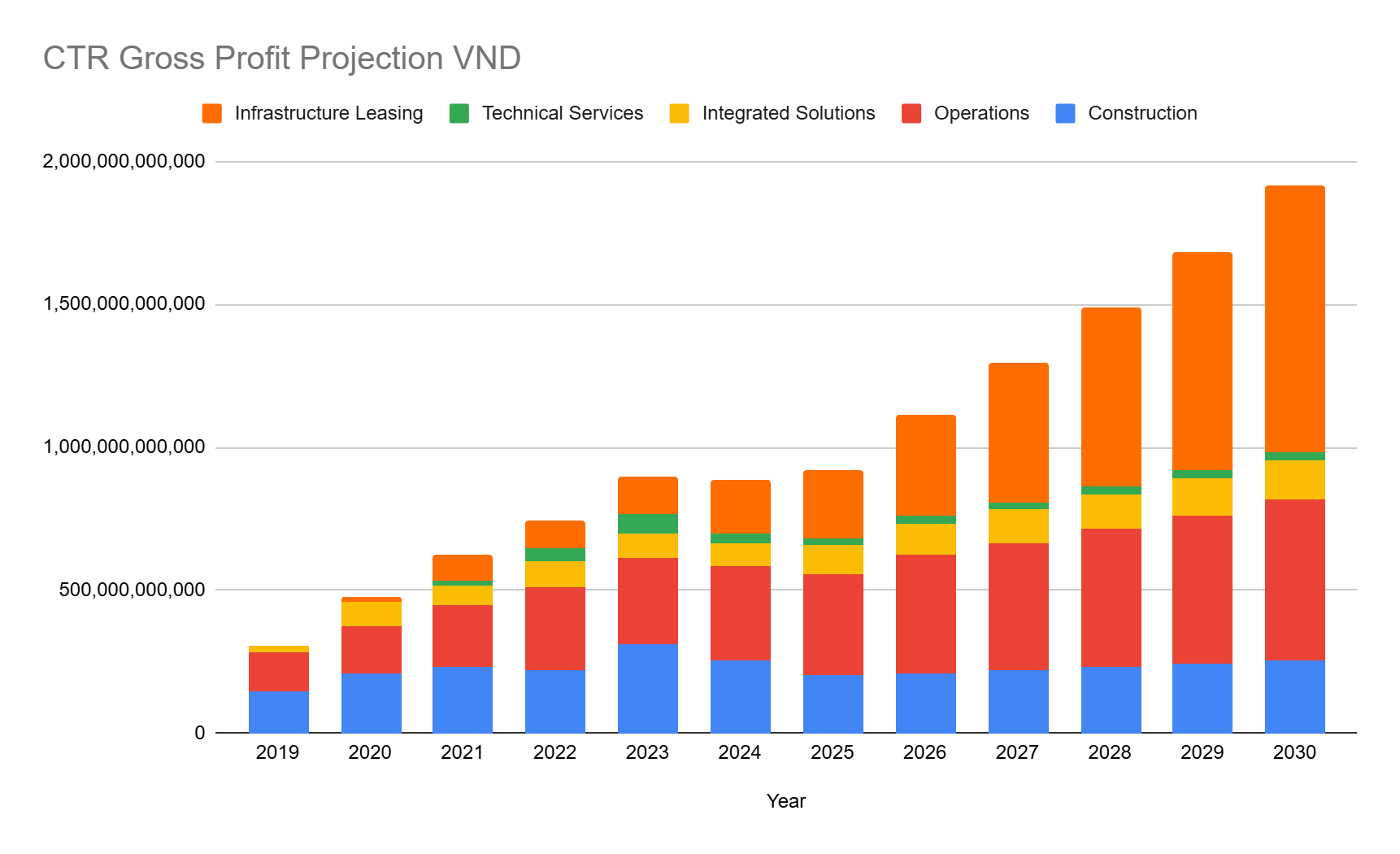

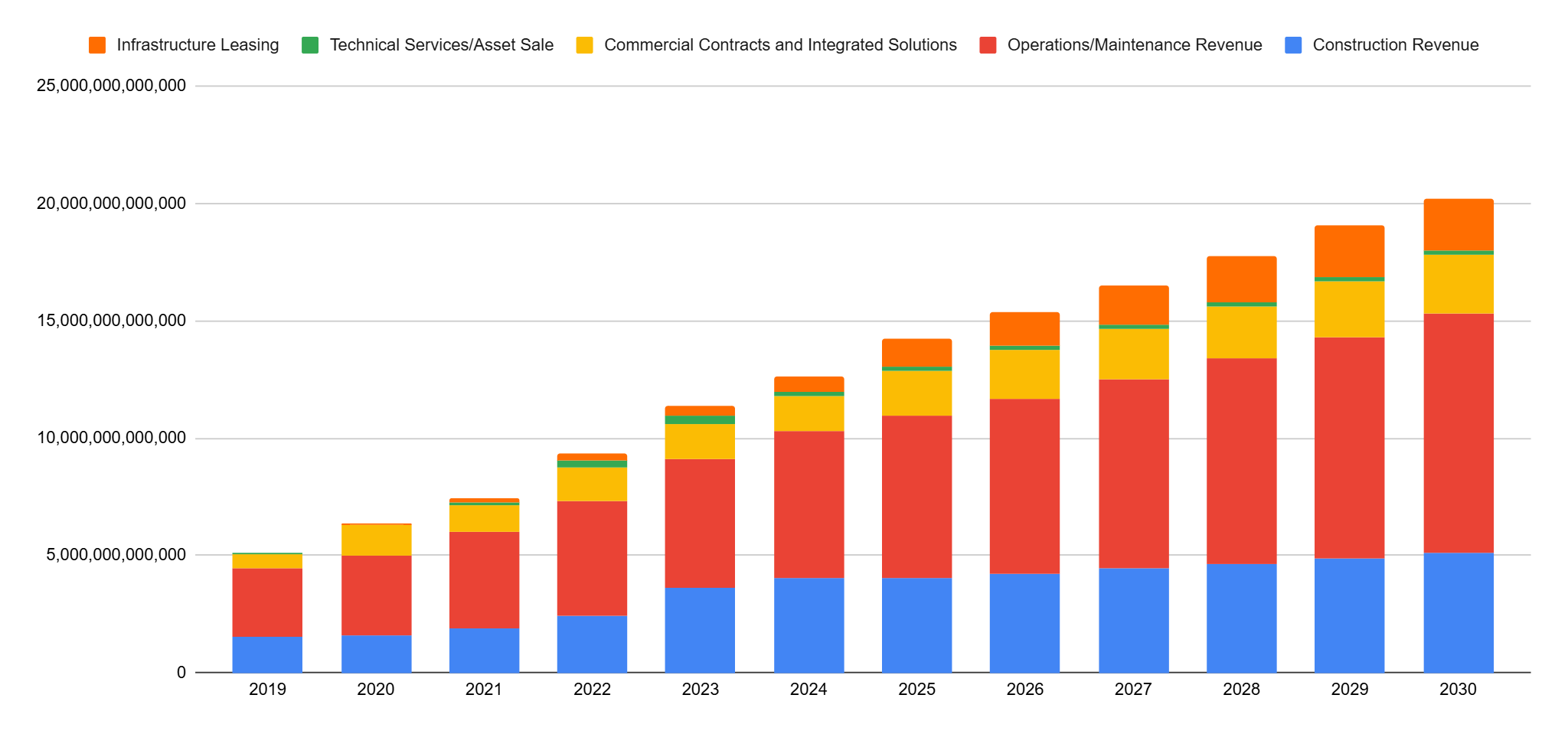

Below shows my quick and dirty estimates for gross profit breakdown over the next 5 years. Here, I am assuming the tower business reaches 1.15 tenancy by 2030 with 20% 2-tenant discounts.

Revenue will remain a small part of the company but a big part of the bottom-line:

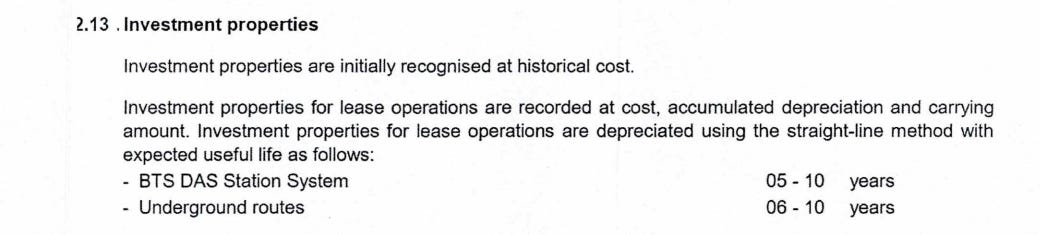

On a side note: seems like CTR is depreciating tower assets at a smaller useful life than the norm. For reference, American Tower had historically depreciated tower assets on 20 years useful life, and since 2024 has extended it to 30 years.

Below is from CTR’s Q3 2025 financial statement:

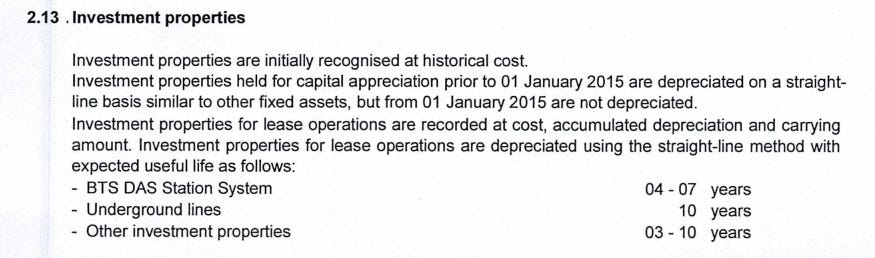

We can even see CTR themselves extending useful life. Check out FY 2024:

We can assume a lower useful life due to many factors including quality of structure, material, equipment, etc. But suffice it to say I believe the high depreciation is understating tower gross profits as in this case depreciation is part of cost of sales.

Nevertheless, even though I am expecting strong earnings growth, there are risks to consider.

While the development of communication points to the state’s desire for tower sharing, MNOs still see their towers as strategic assets and so they want to own the infrastructure they need to grow. I do not know how long it will take for the MNOs to wake up.

There is a key conflict of interest. Since CTR’s biggest client is its majority shareholder, there is pressure for CTR to provide steep discounts to Viettel, preventing CTR from exercising pricing power. CTR already gives Viettel a discount, charging 7.1M VND/month instead of the 8-12M VND/month most would be charging.

Despite strong evidence of local NIMBY resistance to towers, without clear regulation preventing cell towers from being built near each other, then the local monopoly is much smaller than benchmarks like American Tower.

Even though Vietnam may be heading towards a more regulated shared-infrastructure market, right now, I feel like the economics are just not as good as other tower cos, and so I don’t think if CTR deserves an >25x EBIT multiple like American Tower where their towers benefit from far strict zoning requirements, NIMBY, and high tower sharing among MNOs.

At 16x 2024 EBIT, CTR remains in my watchlist.

Still, I think it has the potential to be a great business so will be posting an update if I change my mind, which may be sooner rather than later.

If you think I am wrong. Please challenge me in the comments.

Let’s learn together :)

Great article. You earned a subscription. By the way I am trying to build my own account right now. Maybe you can check it out and give me some feedback