Investment Summary: 2025 research review

Updates on stock write-ups + holdings

Dear readers,

I recently graduated from college and decided to visit family in the Philippines; I haven’t been back in years. As a result, I took a short break from writing over the past few weeks, which is why there haven’t been any recent posts. I started Dunamis Investing as a pseudo-logbook of my ideas but it was only in the past 6 months where I decided I wanted to put more time and love into this blog. As such, I’ve been posting more frequently as opposed to just 2 mega deep dives a year lol, expect this to remain the case.

The portfolio, now completely comprised of small and micro caps outside North America, returned 50% this year time-weighted. This was driven primarily by Lindbergh and Plus Alpha Consulting. And this performance was pure luck, as if you saw my other note (position screenshots posted), I almost sold my entire Lindbergh position as I intended to in my previous portfolio update.

If there’s anything I’ve learned this year, it’s to not sell good businesses!

Since starting this blog, 2 out of the 6 stocks pitched have generated returns above 100%. However, because I’ve been cutting the flowers and watering the weeds, I’ve left a lot of return on the table.

But on the bright side, I also learned you don’t need a lot of multi-baggers to produce strong performance given you have a concentrated portfolio.

Now I’m gonna give a brief update on my portfolio holdings:

Plus Alpha Consulting:

There is talk over AI potentially disrupting SaaS. I think I generally agree with Mark Leonard’s thoughts: it’s hard to tell. AI will increase the ability of SaaS to provide improved customized solutions for its customers but may also one day make it extremely cheap and easy for the customers themselves to customize their own systems. This means the switching costs of the system need to be even higher. Talent Palette has thousands of products and embeds years of data from thousands of employees. One of Talent Palette’s main feature is providing analytics and making recommendations, which is built on the back of aggregated data from thousands of companies. An individual firm trying to customize their own HCIM does not have access to the amount of data necessary to replicate what Talent Palette provides.

Plus Alpha had a great year with a 41% increase in operating profits. Net earnings however are only up 5% due to a ¥1.15 billion write-down on some money losing acquisitions. I’m pleased Mimuro has acknowledged these mistakes. Talent Palette has about 32% of the large enterprise market, and I’ve been happily surprised with their ability to increase ARPU despite bears thinking they’ve hit a wall. Plus Alpha trades at 16x 2025 operating earnings following share buybacks.

Lindbergh:

I was skeptical of Lindbergh’s re-focus to the HVAC business as I had originally invested because I liked the in-night technician delivery business (network management and waste). And indeed, the network management business has gone flat, though the waste management business continues to grow strongly. Nevertheless, I remain happy with the HVAC roll-up performance so far.

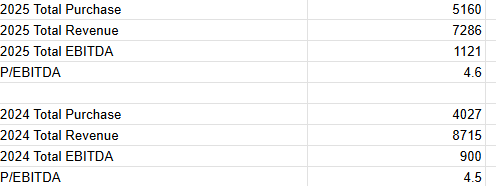

Management has maintained their price discipline, acquiring at an average of roughly 4.5x P/EBITDA (probably <4x EV/EBITDA) for both 2024 and 2025.

*source: LDB press releases

While I expected EBITDA margin uplift to be 10 to 15% post-synergy, the average margins of the businesses were close to 12% while current EBITDA margins post-synergy are 15.6% — pretty good. The main competitive advantages of the consolidation within certain cities are a larger variety of services for different kinds of brands, machines, and situations, allowing for a turnkey solution as opposed to calling many different teams for different issues. Furthermore, greater revenue per € fuel consumed, per € labor for driving, and per € depreciation per truck leads to stronger and stronger route density that small players cannot replicate.

So far, Lindbergh has made 10 acquisitions with another 2 relatively larger acquisitions on the way to closing. They’ve acquired roughly €15 million in annual revenue before post-acquisition growth. I estimate pre-tax return on invested capital for the HVAC roll-up is around 29% just based on EBITDA profits on current margins (15.6%) divided by announced closing purchase prices.

Unfortunately, there was a 12% dilution from exercise of warrants, though the last exercise period has past so there are no more major potential dilutives. Small consistent stock buybacks continue. Another concern is balance sheet liquidity is lower due to cash used for acquisitions but not at alarming levels and solvency is healthy. The business trades at a low teens multiple, valuation still seems reasonable.

Property Databank:

Results have been in-line with what I laid out in my original writeup. Though the cloud business has grown again at 9%, service revenues have declined due to performance schedule cyclicality. As a result, operating profits were down 13% YoY. Of course, the stock went down even though this is a temporary issue lol.

Feature improvements in web billing, property accounting, work orders, and workflow dashboards have been released. Most of this has been done for “@property” and “@knowledge,” not much new additions for “@commerce”, “@cmms”, and “@iwms”. Also doesn’t seem to be reported progress on the Data Lake project which will serve as their sort-of AWS to better utilize their data for potential data aggregation and property evaluation services. I think expansion into the analytics space would be the right move as it will create a whole new layer of value proposition AI can’t replicate. If Property Databank can utilize its massive “databank” for this purpose, I can see the company becoming more of a CoStar or Bloomberg-esque business.

Like Plus Alpha, I believe the high data embeddedness will be a deterrent for existing customers to switch to their own AI-customized solution. Furthermore, due to EDINET compliance and accounting requirements, I can imagine REITs who trust their current provider would have a hard time justifying revamping their system. However, I think it is possible for potential customers in the future to increasingly opt for their own in-house solution as AI becomes better and better and building workflows. Still, “@property” remains an extremely mission-critical product for units and facilities all over Japan.

Overall, decent results and am expecting the stock to rebound once the service earnings normalize. The Japanese real estate DX space still lags behind other developed nations and I continue to be invested in Property Databank’s goal of digitizing the whole life cycle of managing real estate assets.

Ginebra San Miguel:

Net sales up 7% YoY for 9 month period primarily from price increases while sales volumes were pretty flat. This trickled down to earnings growth of 17% and EBITDA growth of 19%. I will be vigilant on capital reinvestment or dividend plans management undertakes.

The recent flood control corruption scandal will have no effect on the brand equity of Ginebra.

I am not particularly excited about the Philippine economy. Though there is strong domestic consumption partly on the back of overseas remittances, but the extremely high levels of corruption has directly reduced FDI and planned infrastructure improvements/buildout.

I think the majority of PH stocks suffer from poor governance and little incentives to grow the business and generate returns rather than just dishing out dividends and sitting on a large pile of cash. There are also many cases of insider stock manipulation due to the extremely low trading volumes. Ginebra is currently the only stock I like in the Philippines as the brand equity is too strong to ignore. I am open minded to adding more PH positions but right now it’s quite likely Ginebra will be the only PH stock in my portfolio for a long long time.

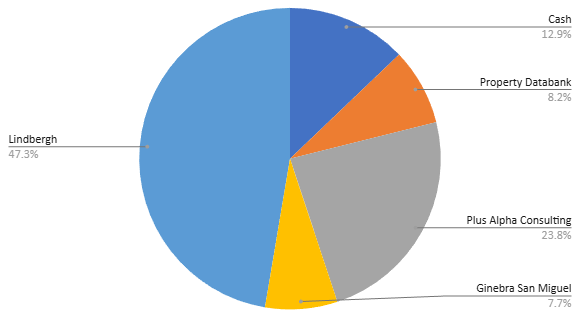

This is what my current portfolio looks like as of writing. No plans to sell any positions right now. Will be reserving existing and additional cash for either additions to Ginebra or 1-2 new investments potentially in Vietnam.

Random thoughts:

The S&P500 has done phenomenally over the past couple years as it has been heavily weighted to AI-related stocks. From what I’ve gathered it seems like the American market is in a bubble (good read by Howard Marks). Nevertheless, I’m not smart enough to know where the technology and valuations will be going in the next several years and I’m happy my portfolio is agnostic to the index.

It’s like fishing in your own little pond rather than competing with thousands of anglers in the most popular lake. There might not be as many fish but they’re a whole lot fatter. As someone once told me, you need to choose a game where you have an edge. Isn’t it great that we can choose our own game?

I find my edge inching further towards the small cap space, primarily in Asia.

Small companies are overlooked and provide opportunities to find undervalued compounders.

However, there is an issue I have with small and micro caps which prevent me from investing in most of them:

More often than not, small companies, because they are small, lack the competitive advantages to dominate the market.

In many stocks I look at, my biggest question is are they better than their competitors? And are they going to become monopolies?

In many cases size is power.

Scale advantages come in many forms ranging from cost savings to talent to data. I usually buy a company that has the leading market share or whom I believe is strong enough to eventually have the leading market share.

Applying this to the small cap space, I only buy companies that dominate a small market.

Take Lindbergh for example, they have a dominant market share among Italian technicians and Italian HVAC. They aren’t trying to become DHL, nor are they serving the entire multi billion euro parcel logistics space. Instead, they focus on a niche, and serve that niche the best.

Similarly, vertical market software companies are excellent candidates as they create local monopolies only WITHIN their vertical. Property Databank is a 62 million dollar company yet has majority market share among large property developers.

So it’s less about the size of the firm and more about their size relative to the overall market/niche.

A lot of small and micro caps I find are extremely cheap and could very well make huge returns, but they also compete on the same plain with billion dollar juggernauts who have scale advantages and talent that these small businesses can’t possibly compete with.

The trick for these companies then is to be different.

A small company facing a giant can win if they do something better than the competitors. But that’s not all, this differentiation needs to be hard to replicate.

It’s hard to be different if you are selling a commodity. For example most microcap factory stocks in the SEHK are selling the same product everyone else is selling. There’s no competitive advantage.

So in summary, through the lens of quality, the way you study a large company like Apple and Amazon, is no different than how you study small companies. It still has everything to do with the competitive advantage:

How sustainable is the competitive advantage?

How insurmountable is the competitive advantage?

How replicable is the competitive advantage?

As this year I narrowed my focus on benchmark investing, I’d like to go over some honorable mentions that I did not invest in:

Gemadept

As part of my Vietnam research, I was highly interested in ports as a means to capture the growth in the manufacturing and export boom the country has and will continue to experience. However, I realized most of these ports were poorly run and state-owned. Some faced intense competition with neighboring ports while others such as the Danang Port could potentially lose its business as the government plans to build a replacement port right next to it. Hence, Gemadept seemed really interesting as it was one of the few local private port operators and had several port concessions in both the north and the south. They had good growth and the stock was trading <20x earnings. However, I was disappointed to see huge share issuances as management kept raising equity to fund projects, diluting existing shareholders.

Inter Cars

Since I knew about AutoZone, I was interested in Inter Cars, a Polish spare car part distributor dominant throughout Europe. Thus my quest to determine if Inter Cars was European AutoZone began. Now I believe what made AutoZone so great was a combination of its negative working capital and its SKU variety. If you are driving and you get into an accident, you want to fix your car ASAP. Ergo, as a workshop you need to be able to get whatever the customer needs within hours (same if you are DIY). But cars have many parts, and different brands have their own specifications. So as a distributor you need to have ALL KINDS of SKUs in inventory in PROXIMITY to the workshop or customer to be able to provide the items they want. T

here’s just one problem, inventory = working capital. If you’re a new entrant, how on earth are you going to stock enough of tens of thousands of SKUs in each store/warehouse? You can’t. So Auto Zone’s scale advantages enable them to have an extremely low inventory turnover yet high ROIC per location as they are able to provide a greater variety of items that the workshop needs at a faster delivery time leading to customers choosing them over competitors.

As AutoZone buys so much parts from many different producers and brands, they develop negotiating power against their suppliers. With superior credit ratings, they can essentially stock their stores without any initial cash outlay: negative working capital, allowing them to scale up at a pace smaller players cannot.

And that’s what made AutoZone such a great business. Suffice it to say I did not find the same dynamics or high ROIC unit economics take place for Inter Cars or its other Polish rival Auto Partner. In America many people travel HUGE distances and oftentimes you might get stuck in the middle of nowhere. The urgency of getting that spare part is higher. You also have a major DIY culture in America which is a big part of AutoZone’s business.

Union Auction

I discuss both of these in a previous post. Union Auction is the leading Thai vehicle auction house that had gone digital trading at 10x earnings. I was initially excited about Union Auction as it had parallels with Copart, another online auction house that was a huge compounder and excellent business. However, the key difference with Copart’s moat is that they own the land whereas Union leases. Due to the high regulatory barriers to set up a salvage yard, the best land is limited, and owning the land means perpetual access to this scarce resource. Since Union leases their land, they can be outbid at renewal and so their advantage is eroded. As such I don’t believe they have the characteristics that made the Copart economics so great.

Yes Asia

A fast growing online distributor of Korean, Japanese, and Taiwanese beauty products that was trading at 9x earnings when I looked at it. It was riding the wave of K-beauty and had the largest market share for international online K-beauty products. However, I felt the business wasn’t that great as competitors had managed to undercut Yes Asia in price. I felt the customer experience and website were marginally better but in the end, Yes Asia felt more like a run of the mill reseller. Their new B2B wholesale business is susceptible to the sellers and buyers cutting out the middle man as I find no strong sense of “one stop shop” effect for their wholesale buyers.

Grand Banks Yacht

Grand Banks was trading at 2x earnings and was well regarded in the yacht space. What prevented me from making the buy was I was concerned about the cyclically of the business, particularly that as Grand Banks is an ultra luxury good, it would be extremely susceptible to wealth decline. Grand Banks also sells just a few ships a year meaning sales can are extremely unpredictable. I’m also not sold on Grand Banks mindshare as I’m not a yacht owner myself so I felt like GB was no different than other classic yacht brands.

Credit Bureau Asia

Monopoly credit issuer and is a part-owner of the central credit scoring system in Singapore. But don’t have the conviction to pay 30x earnings for this business.

Will be releasing a research update as soon as possible on Vietnamese companies I’ve been interested in. I think there’s still a lot of due diligence I need to do, and to be honest the progress has been a bit slow recently. Will try to get a preliminary write-up in a week or two.

Thank you for reading, Merry Christmas, and happy New Year. Please subscribe if you’d like to follow along my investment research.

Thank you! Very interesting. Your journey with Lindbergh seems to have paralleled mine... :-)

Very good thoughts! I will follow your journey! I really liked the part about small companies and competitive advantages.