Plus Alpha Consulting - Part 2

a piece of the Japanese cloud revolution for just 11x ebitda

Note: A hiccup in Part 1 which has now been updated was I didn’t break down the operating margins of the HR solutions segment. Talent Palette has a 50% operating profit while consolidated HR solutions segment has a 40% operating profit. Consolidated Plus Alpha operating profit which includes company-wide corporate overhead is 33%.

Thanks and Merry Christmas!

—

This is part 2 of the deep dive on Plus Alpha Consulting. If you haven’t yet, please read our general write-up on the company — Plus Alpha Consulting - Part 1.

As we’ve discussed before, Plus Alpha is not just a SaaS company, they are at heart a text mining company. To reiterate, text mining is an application of machine learning that enables the analysis and interpretation of any text or language input through big data models. Plus Alpha is in the process of making the transition from having a machine-learning focus to an AI focus. We believe because Plus Alpha has been a text mining company since the beginning, the transition will be a lot easier and a lot faster than most average SaaS companies.

Additionally, while our analysis is mostly centered on Talent Palette, we don’t want to ignore the potential future free cash flow that could come from Plus Alpha’s other products.

Let’s start by turning our attention to Plus Alpha’s other existing offerings: the marketing solutions.

Mieruka-Engine allows firms to use text mining to analyze and visualize customer feedback from direct forms, call logs, or social media. The tool can scan text and voice data, pinpoint key words, interpret feedback results, and more.

Mieruka-Engine is more of a tool than it is an enterprise software. It lacks the feature richness, data integration, and mission criticality of Talent Palette. Customers mainly use Mieruka-Engine as an add-on to their existing CRM systems.

Mieruka-Engine is unique in which there are very few similar products that do text-mining for customer analysis. It seems like a good product overall from the feedback we hear, but customers are definitely a lot more price sensitive.

The second marketing SaaS product, Customer Rings, allows firms to analyze and visualize customer purchase histories, web access logs, etc. They also serve as a CRM system where users can manage email campaigns, SMS bots, feedback forms, and dynamic website graphics.

We like Customer Rings more than Mieruka-Engine, mainly because getting on the system requires integration with all customer and marketing data as opposed to just feedback results and log data. In fact, it takes about 1.5-2 months to set up for large enterprises in order to log in all the data. There is also a moderately large variety of functions, with most of the value proposition coming from the data analysis and visualization tools. Better switching costs, but the CRM space is by far the most crowded vertical.

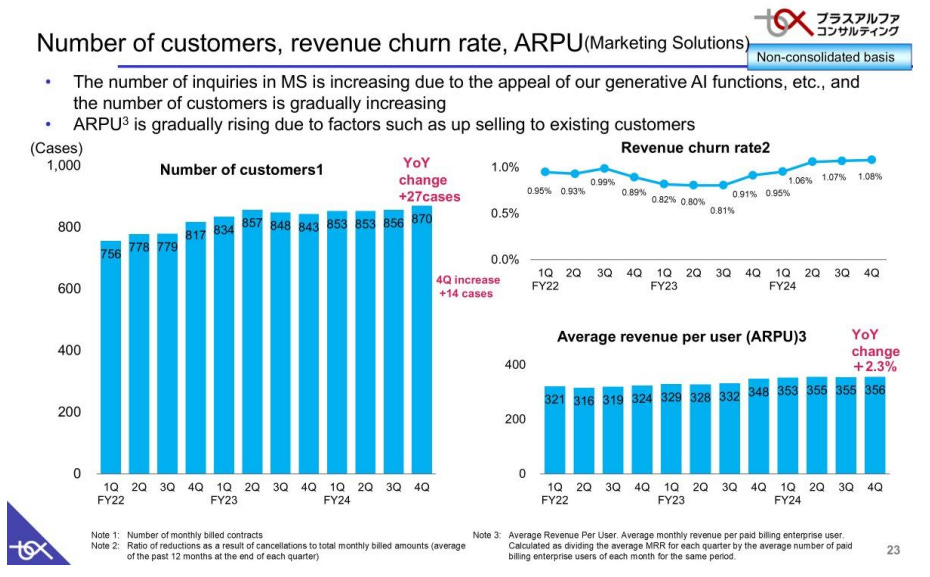

Overall, the marketing solutions have ok economics. There are 870 customers, mostly mid-size and large enterprises. Customer base has grown just 5% YoY for the past several years. The product is generally on the expensive side, ARPU stands at ¥355k, increasing 4-5% YoY. MRR churn rate is pretty high, averaging 0.9-1%, over triple that of Talent Palette. Most churn comes from cancellation due to price increases, which tells me the marketing solutions are generally less mission-critical and face tougher competition.

Mieruka-Engine YoY growth has stayed at 4-5% for the past 4 years, Customer Rings on the other hand has grown >10% per annum over the same period. This is in part because Customer Rings has an established distributor network compared to Mieruka. However, Customer Rings has worse profitability with an operating margin of about ~30% while Mieruka has averaged >50% because Mieruka is a simpler product and doesn’t require as much infrastructure or customer support.

In summary, a highly profitable business, but with mediocre expected growth for a SaaS business.

—

While not important to the thesis, It’s also worth talking about something we believe could range from a slight negative to very large positive:

Mimuro has been launching multiple products related to text-mining since he started the company. Most of them were in the marketing space, and most did not stick. To this point, Mimuro has not stopped, and with valuable experience from his past failures and success of Talent Palette, Mimuro has been up to some very interesting new projects. While most will fail, even one success could lead to a homerun……

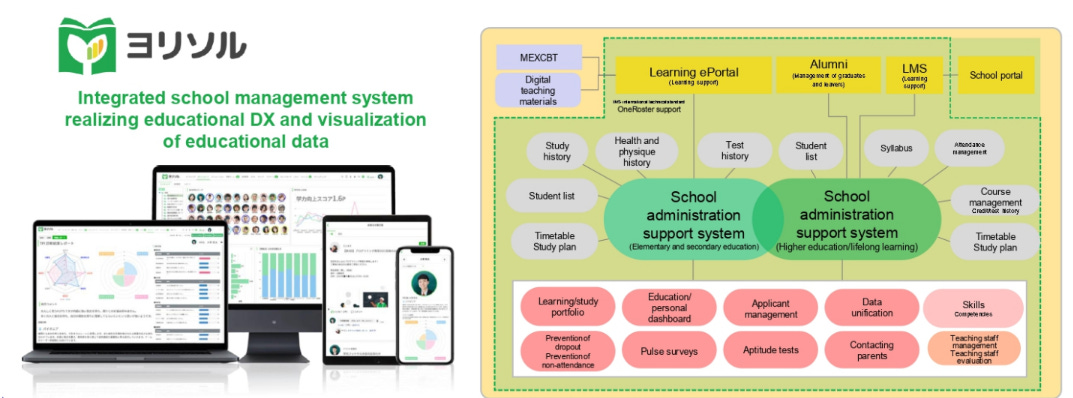

Mimuro launched Yorisoar in 2022. Yorisoar is a learning management solution (“LMS”) for schools and universities that helps with managing teachers, classes, and students, with a variety of features from staff attendance and grading tools to student performance analysis with Plus Alpha’s signature big data analysis tools that can help teachers understand what students need to improve, help them get jobs or get into their desired university, or prevent them from dropping out.

Like Talent Palette, Yorisoar is a mission-critical system that integrates with the entire organization of the user. Teachers, students, and administrators require the use of Yorisoar for everyday school activities.

There are some synergies Yorisoar can provide to Talent Palette which Mimuro has pointed to. Utilizing the student data from Yorisoar and the employee data from Talent Palette can help better match employees with employers. In late 2022, Plus Alpha acquired Grow Up, a ¥600M revenue HR SaaS company whose main product is Kimisuka, a tool that helps match companies with job applicants. This will provide the infrastructure to eventually bridge the gap between Yorisoar and Talent Palette (Mimuro acquired Grow up for about ~8x 2024 operating profits. Compare that to Kaonavi’s acquisition of Work Style Tech for a high single digit sales multiple. Both companies were unprofitable at acquisition with the same M&A motivation to incorporate the acquiree’s features).

Yorisoar was used by 10 schools in FY2023, expanding to 70 schools this year with an ARPU of ¥170k. Plus Alpha is targeting to expand their customer base by 40-50 new schools a year. Yorisoar currently generates ¥142M in annual revenue with a -¥166M operating profit.

Among universities, the LMS space is already very crowded. LMS software was widely adopted during the pandemic which forced schools to offer classes online. >70% of the roughly 800 universities in Japan are already using LMS software. Moodle and Manaba are the largest players which together likely command >50% market share.

The main opportunity is within high schools and vocational schools which likely have lower ARPU but are still mostly unpenetrated.

Don’t get your hopes too high though, a declining population means less and less kids in school. Nevertheless, the roughly 15,000 high schools and 2500 vocational schools in Japan makes for a pretty wide addressable market. And it seems that Yorisoar has generally performed better than management expected.

—

Also in 2022, Plus Alpha released Sales Square. Sales Square is essentially a combination of Talent Palette and Customer Rings — a HRM and sales management solution for sales and support teams. Sales Square allows companies to manage sales skill development, manage and track KPIs, manage leads and cases, build forecasts, and analyze and visualize marketing data. It’s a very small operation and there’s not much disclosure on Sales Square so far.

Aside from these two, Plus Alpha also just soft-launched a cloud hospital management system called HiCare Wellness which utilizes text-mining and GenAI to help improve patient experience and manage doctors/nurses/staff.

Only time will tell how these new ventures add contribute to the consolidated business. But it’s a positive to see this failure-is-learning mindset that we feel is kinda rare for a Japanese company.

Mimuro: the man behind the curtains

Ex-employees describe Mimuro as quiet and analytical, and the work culture has been described as “venture-like”. Rules are looser. Unlike most traditional Japanese companies (often referred to as black companies), the work hierarchy is quite decentralized. Employees at Plus Alpha are given significant amounts of autonomy to come up with their own ideas and suggestions. When employees come up with a new idea, they are given 2 months to build and implement — people are expected to fail fast. This kind of work culture is imperative in a business where innovation is key.

Though management are only paid with a salary, we think there’s sufficient skin in the game as insiders own 40% of Plus Alpha. Mimuro himself owns 21%. VP Kenji Suzumura, who was at Plus Alpha since the beginning and was best friends with Mimuro while they were at Nomura, owns 16%.

In some aspects, capital allocation is similar to most Japanese firms — fat cash balance, no debt, dish out some dividends. Japanese businesses have been notorious for being very risk-averse when it comes to capital allocation.

Plus Alpha hasn’t really done much with cash flow until the past couple years when it started making several acquisitions. Aside from Kimisuka, Plus Alpha made 3 acquisitions this year:

Attack Inc. is a recruitment service and consulting business. They were acquired for ¥80M at 0.47x sales (unprofitable). Plus Alpha wanted Attack to expand their consulting team, acquire their customers, and increase expertise in recruitment.

D4DR is a business consulting and IT transformation business. They were acquired for ¥144M at 11x after-tax earnings. Like Attack, Plus Alpha’s motivation is to use D4DR to provide customers, talent, and use their data to improve their products.

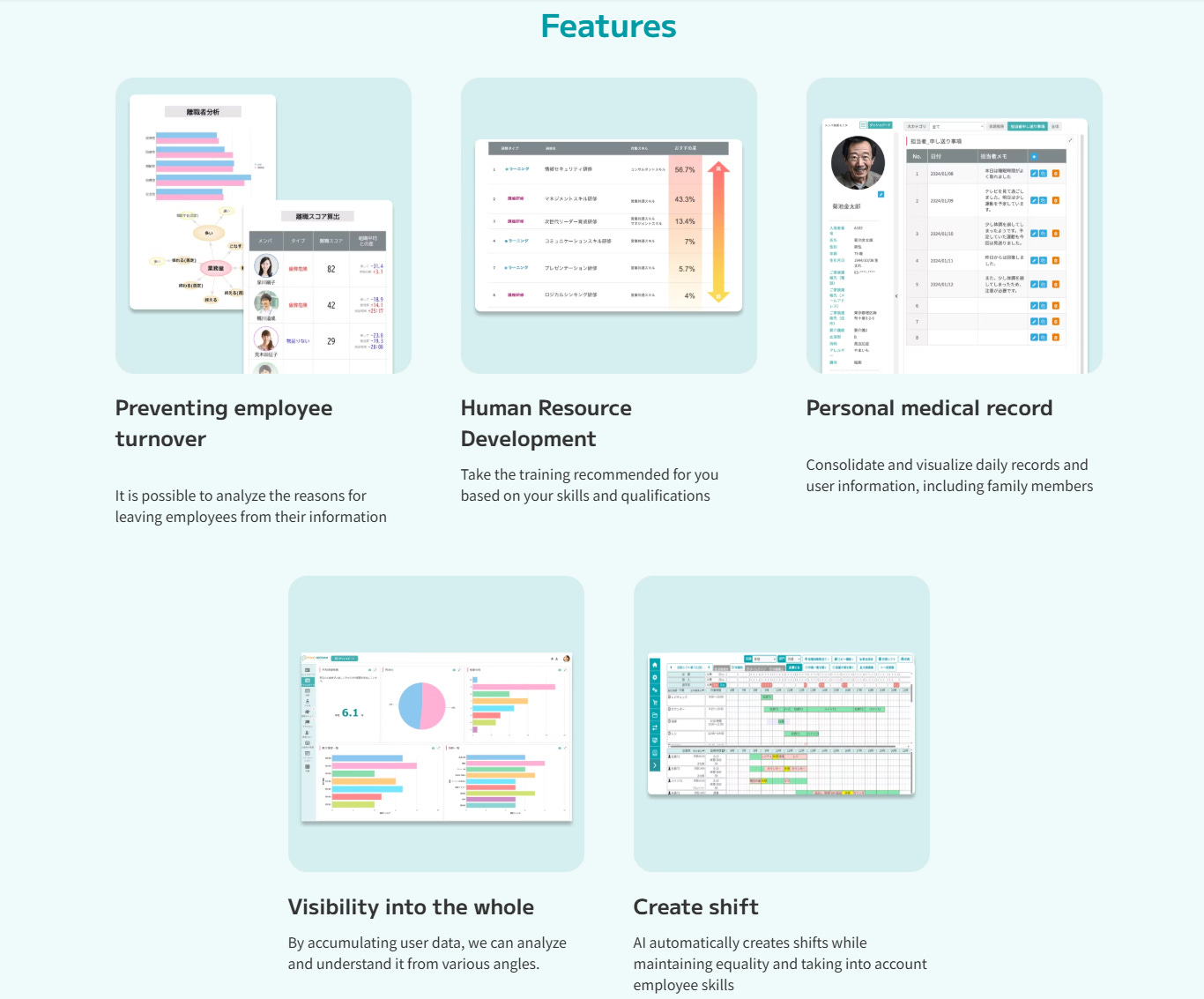

OMN was Plus Alpha’s largest acquisition for the year. OMN’s main product is R-Shift, a service that uses optimization to match the number of employees required for each store/branch with the available working days and hours, skills, and experience of the employees. They also provide shift management, payroll management, and budget management. Plus Alpha wants to incorporate OMN’s software into Talent Palette. OMN was acquired for ¥1.6 billion at a 6.6x operating profit multiple.

Acquisitions are mostly product and expertise led. We think management is pretty disciplined as all the acquisitions so far have been made at reasonable or cheap multiples, though they’ve used some stock issuance to fund the purchases resulting in a 6% dilution since IPO.

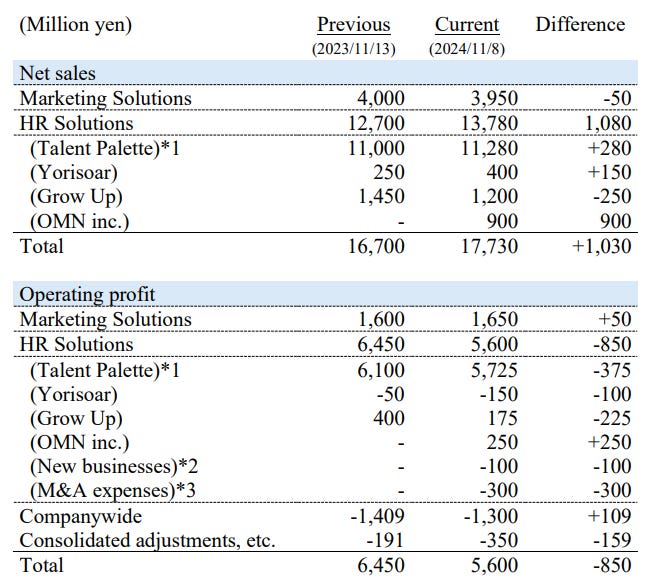

Figure: changes in 2025 projections

So far, Kimisuka has been a bit of a hiccup, generating only ¥177M vs their projection of ¥300M in operating profits. Further M&A-related costs, unprofitability in new product launches, and more aggressive discounting for Talent Palette have resulted in 2025 guidance revised down.

But the market is throwing the baby out with the bathwater. Sure there will be hiccups, just like any company, but 5 to 10 years from now, none of this will matter. All we know is Talent Palette will continue to dominate the TMS space. Management seems to agree as they’ve recently announced a share buyback of nearly 6% of shares outstanding in response to the sell-off — a positive sign that management recognizes the stock is undervalued and has consequently taken action to add value for shareholders.

Valuation

Plus Alpha is valued at ~11x 2025e ev/ebitda, likely ~10x when counting the share buybacks. (Price/2025e FCF of ~19x, ltm ev/ebitda of ~14x).

This is a historic low compared to the >20x ntm ev/ebitda Plus Alpha used to trade at over the past few years. Moreover, Kaonavi trades at close to ~25x forward ebitda (though they trade at a much lower revenue multiple due to lower profitability). Other profitable ERP software companies like OBC also trade above 25x.

Even when you mix in the lower quality marketing segment which rightly should have a lower multiple, Plus Alpha still seems quite cheap. Furthermore, as Talent Palette outgrows the marketing business and other solutions, overall profitability will likely go up.

If this company was in America, we wouldn’t doubt this could trade at above 20x ntm ebitda easy, as has been the case with Salesforce and Workday since IPO, and remember that these firms have much larger dilution from share-based compensation.

In summary, we think 11x forward or 16x ltm ebitda is a substantial discount for a wonderful software business with high switching costs + a customer base that absolutely adores the product.

If Talent Palette can grow customer base at 15-17% with flat ARPU growth and zero margin uplift, they would end up with ¥8 billion ($51 million USD) in just 4 years. As Talent Palette outgrows the Marketing solutions segment and assuming everything else grows very modestly, we estimate the whole business can easily grow ebitda by at least ~18% for the next several years with an operating profit of ~35-37% — about ¥8.8 billion in EBITDA; slapping on the same growth rate on the cash pile, we end up with ¥19 billion in cash.

Applying a 20x EBITDA multiple gives us an IRR to our estimated value of >25%. If Plus Alpha ends up with the same multiple it has now, you still get an IRR of ~18%!

Conclusion

Plus Alpha Consulting through Talent Palette provides an opportunity to invest in a fast growing talent management enterprise software with extremely high switching costs and robust unit economics all in a highly unpenetrated space facing ever increasing demand for software. And because of Mimuro’s continuous commitment to developing text mining and gen-AI vertical software products, new growth opportunities could be near endless!

Very good writeup. Really appreciate it. I would love to know how you were able to find so much info on the company and management, etc... I did some digging myself before (reading Q&A transcript, briefing, interviews with management, news, google search, etc...) and definitely not able to find so much useful info as you. If you could point out how you were able to find so much of such info and insights on Japanese companies, I would really appreciate it. Thanks in advance.